Future-proof your business in 2025

Learn how to tackle challenges and opportunities in 2025 with actionable advice and tips on international payments. Adapt your business to the year ahead.

If 2024 was anything to go by, changes affecting the business environment will keep coming hard and fast in 2025. According to Accenture’s 2024 index indicator, the rate of change has been increasing over the past six years when looking at factors such as technology, talent, geopolitics and climate, and spiked in 2023 when generative AI was introduced.

For SMEs starting to plan for next year and beyond, it may seem increasingly difficult to keep abreast of new developments and business technology trends. From the Accenture report, over half of surveyed business leaders said they weren’t fully prepared for potential changes.

However, there are actionable strategies that business owners can rely on to ensure long-term success, such as prioritising adaptability or reassessing business objectives and operations to stay aligned with market demands. Here’s what to do to stay ahead.

Remain flexible

Winston Churchill once said, ‘I never worry about action, but only about inaction’ and the same goes for business. In a landscape that’s shifting rapidly, the ability to adapt and make decisions quickly is often the difference between businesses that survive and those that thrive.

Wrimes Cosmetics, a face paint brand and WorldFirst customer, had to pivot during the pandemic, developing a range of pet care products that’s now globally recognised. And many companies, from Play-Doh to Netflix have seized opportunities or responded to market trends to become the brands we know today.

Flexibility starts with mindset. Businesses that foster a culture of adaptability – where teams feel empowered to experiment and embrace change – tend to respond more effectively to challenges. For example, being open to rethinking how you use technology or restructuring team to focus on emerging priorities can help you achieve your business goals, whether that’s launching a new product, automating tasks or reaching a new audience.

It also means staying informed. Keep an eye on trends in your industry, listen to customer feedback and maintain regular communication with suppliers and partners. This will help you anticipate changes and adapt, rather than react.

Review partnerships and operations

As the new year approaches, it’s a good time to examine the partnerships and operational processes that drive your business. Relationships and workflows that may have been effective in the past might no longer align with your current goals or the changing market environment.

For example, as a growing business, manual processes that were feasible in the past may now be subject to errors and delays with an increased volume. While there’s an initial investment to upgrade to an automated system, ultimately, this would free up time and staff to focus on more strategic tasks.

Or consider whether your suppliers have responsible business practices that align with your values. If your customers are questioning your environmental sustainability but your long-time supplier is slow to adopt more eco-friendly processes, continuing the partnership could harm your reputation and alienate your customers.

Assess your key partnerships

Your partnerships – with suppliers, service providers, and even customers – play a vital role in your business’s success. Questions to consider include:

- Does your supply chain management ensure reliable delivery times, quality, and cost-effectiveness?

- Do your suppliers or service providers align with your values, such as sustainability or ethical sourcing?

- Are you receiving fair value for money from service providers, or are there better alternatives available?

- Are there any contracts or agreements that could be renegotiated for better terms?

- Are there customers or partnerships that are no longer profitable or align with your target market?

Evaluate your internal operations

Operational efficiency is key to maintaining productivity and scaling your business, with a report showing that some businesses are losing up to US$1.3 million per year due to inefficient processes.

Here are some questions to ask:

- Are there repetitive tasks that could be automated to save time and reduce human error?

- Do your current tools and systems meet your team’s needs, or are they outdated?

- Are communication and collaboration between teams effective, or do silos exist?

- Are you consistently hitting deadlines and providing an excellent customer experience, or are delays common?

- What operational processes are causing unnecessary stress, delays or errors?

Work with a business mentor

If you’ve found yourself uncertain about how to drive your business forward, a mentor can provide fresh perspectives, actionable strategies and the confidence to tackle your biggest challenges. Unlike a business coach who may focus on more specific, short-term goals, a business mentor offers long-term guidance and valuable insights, as they’ve experienced the ups and downs of business themselves.

A business mentor acts as an advisor in this beneficial relationship, providing anything from strategic planning, networking, accountability and personal development. Since the nature of the relationship can be quite broad, you’ll need to be clear on what you want to get out of a mentorship. A mentor who’s been in your industry for decades will be able to share practical advice specific to your sector, including spotting new opportunities, while a mentor with a broader business background might focus on transferable skills like leadership or financial planning.

It doesn’t need to be a one-way mentorship either; reciprocal mentorships are more informal and based on mutual benefits such as knowledge sharing or networking opportunities.

To find a mentor, look within your existing network or use the UK Government’s Mentorsme website, which has a database of mentoring organisations in your area. Alternatively, local chambers of commerce, business accelerators and industry-specific associations are valuable resources for connecting with potential mentors.

Invest in sustainability and ESG

In business, sustainability and environmental governance are no longer buzzwords – they’re now baked into the law. The EU’s Corporate Sustainability Reporting Directive (CSRD) came into force in 2023, requiring large enterprises and listed companies to share detailed information on their sustainability impacts, in order to improve transparency and accountability. It also applies to non-EU companies that do business in the EU, and who meet the criteria for reporting.

Beyond legal requirements, though, research shows that sustainable practices and environmental awareness is good for business. One survey showed that half of consumers are willing to pay a premium for products branded as sustainable, while another found that over a third of B2B customers would change suppliers if their sustainability needs weren’t met. And in the UK, 52% of consumers check a brand’s sustainability practices ‘somewhat often’ or ‘very often’.

This sentiment is reflected in the opinion of C-level executives, who see customer loyalty and customer engagement as benefits of incorporating sustainability efforts.

It pays to look at your environmental impact in the broader framework of Environmental, Social and Governance (ESG), since environmental impact, social responsibility and governance practices are often interrelated. These three pillars contribute to a company’s overall resilience and profitability, with studies consistently showing that a company’s level of social responsibility is related to employee satisfaction and retention. While environmental initiatives can overshadow other aspects of ESG, considerations of human rights, diversity and transparency are equally important.

If you’re looking to integrate Environmental, Social and Governance (ESG) into your key strategy, start by understanding where you currently stand.

Environmental

- Audit your impact by measuring your carbon footprint, energy usage and waste output

- Set goals to reduce emissions or switch to renewable sources

- Work with suppliers who meet sustainability standards

Social

- Support employees with wellbeing strategies and professional training

- Improve employee engagement with flexible policies and initiatives

- Foster inclusivity by reviewing hiring policies and build a diverse workforce

- Ensure your partners comply with the Modern Slavery Act and you have full supply chain visibility

- Contribute to community initiatives or support local causes

Governance

- Involve your leadership team in ESG strategies and accountability

- Be transparent and share regular updates on your progress

- Include ESG goals in business decision-making and business growth strategies

Explore new markets

Recent political developments have highlighted the importance of spreading your risk across multiple regions, rather than relying too heavily on a single market. Trade policies, tariffs or economic priorities can shift overnight, leaving businesses vulnerable.

Expanding into new markets and building meaningful relationships with local suppliers, partners and customers will ensure your business is resilient against any sudden changes.

Asia’s prominence in the global economy makes it a region to watch. The five fastest growing economies in 2024 are all in Asia, and Asian countries – particularly India, China and Indonesia – have an emerging consumer class that could provide sustainable growth and steady revenue for years to come.

Meanwhile, in Southeast Asia, Singapore and Malaysia are leading the way in digital transformation. Expanding your footprint in this region is a strategic way to future-proof your business, but growth potential isn’t just about a booming middle class.

Here are some things to consider:

- Ease of business: Are regulations and processes business-friendly?

- Trade tariffs: Will import/export costs affect profitability?

- Market demand: Is there strong demand for your product or service?

- Digital readiness: Is e-commerce and the digital infrastructure growing or well developed? What’s the internet penetration rate?

- Economic stability: Are inflation and currency risks manageable?

- Payments and banking: Can you easily make and receive payments in the local currency? Setting up a multi-currency account like the World Account can help simplify international transactions and improve cash flow

- Competition: Who are the key players, and is there room for your business?

- Cultural fit: Does your brand resonate with local values? Will language pose a challenge?

Financial planning

If your business pays or gets paid in foreign currencies, you’ll understand the toll that fluctuating exchange rates can take on your bottom line. Exchange rates rise and drop for many reasons, including inflation, political instability, speculation and recession – factors that can be difficult to predict. However, using tools like a forward contract or natural hedging can reduce these risks.

Manage exchange rate risks with forward contracts

One way to safeguard your budget is by using forward contracts. A forward contract from WorldFirst allows you to lock in an exchange rate for up to 24 months, giving you certainty over costs; this means that even if exchange rates change, the amount you’ll pay won’t. Whether you’re paying suppliers overseas or bringing funds back to the UK, forward contracts ensure that rate fluctuations won’t derail your financial plans.

Reduce costs with a multi-currency account

Multi-currency accounts like the World Account can also help you manage exchange rate risks. By receiving payments in foreign currencies such as USD or RMB and paying suppliers in the same currency, you can avoid unnecessary currency conversions and their associated fees. This kind of natural hedging acts as a simple way to protect your business from exchange rate swings while keeping costs down.

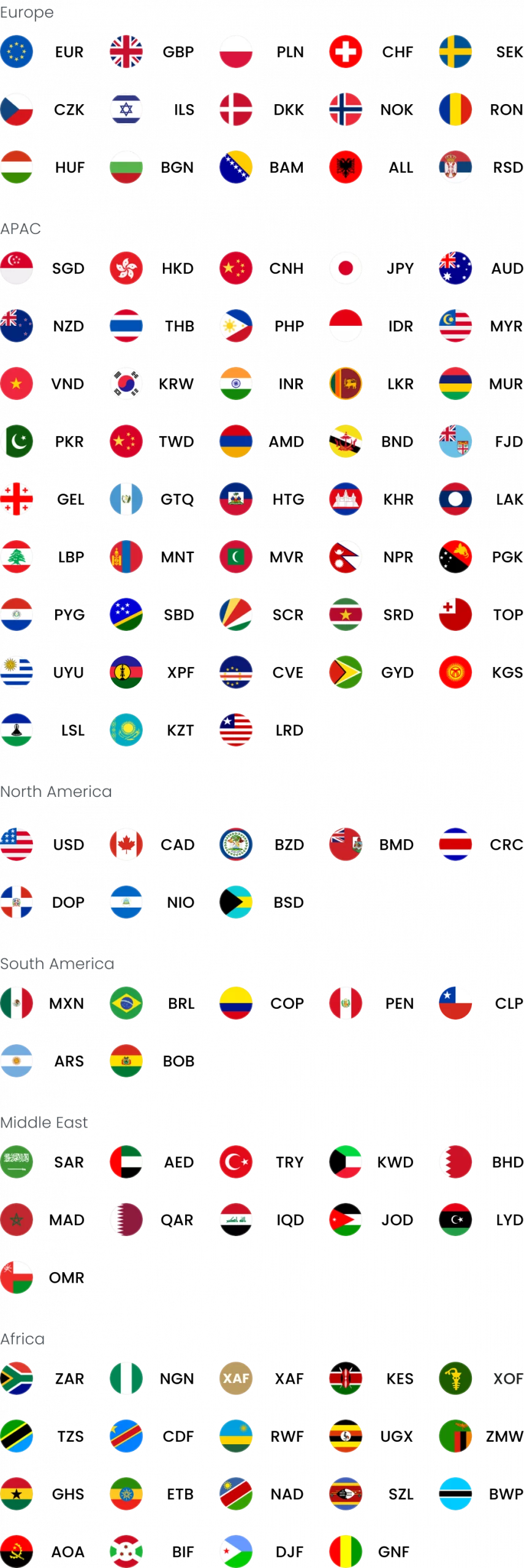

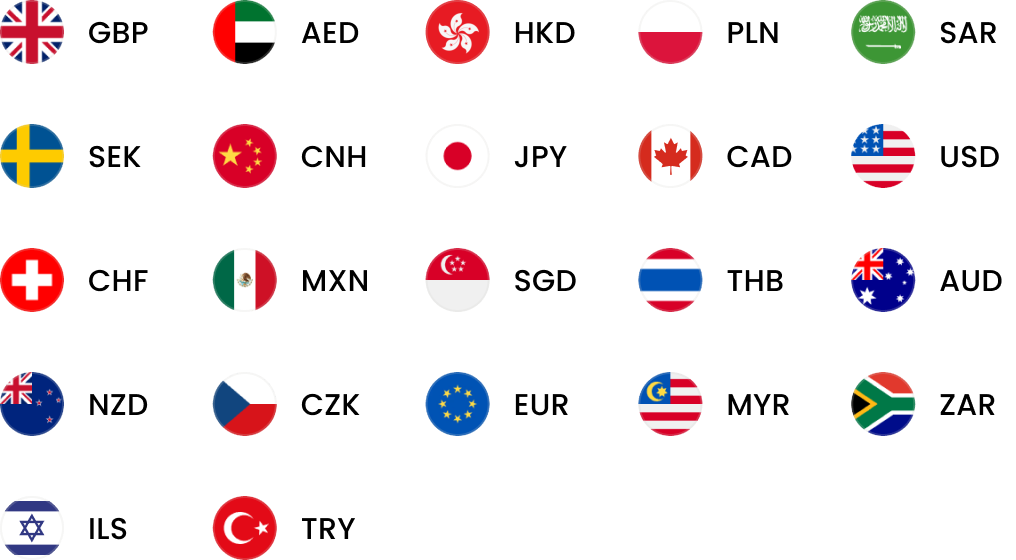

The World Account allows you to open accounts in over 20 currencies and hold balances in those accounts without any fees. It’s free to receive payments and currency conversion margins are capped at 0.5%, while fees are waived for larger cross-currency payments.

- Open 20+ local currency accounts and get paid like a local

- Pay suppliers, partners and staff worldwide in 100+ currencies

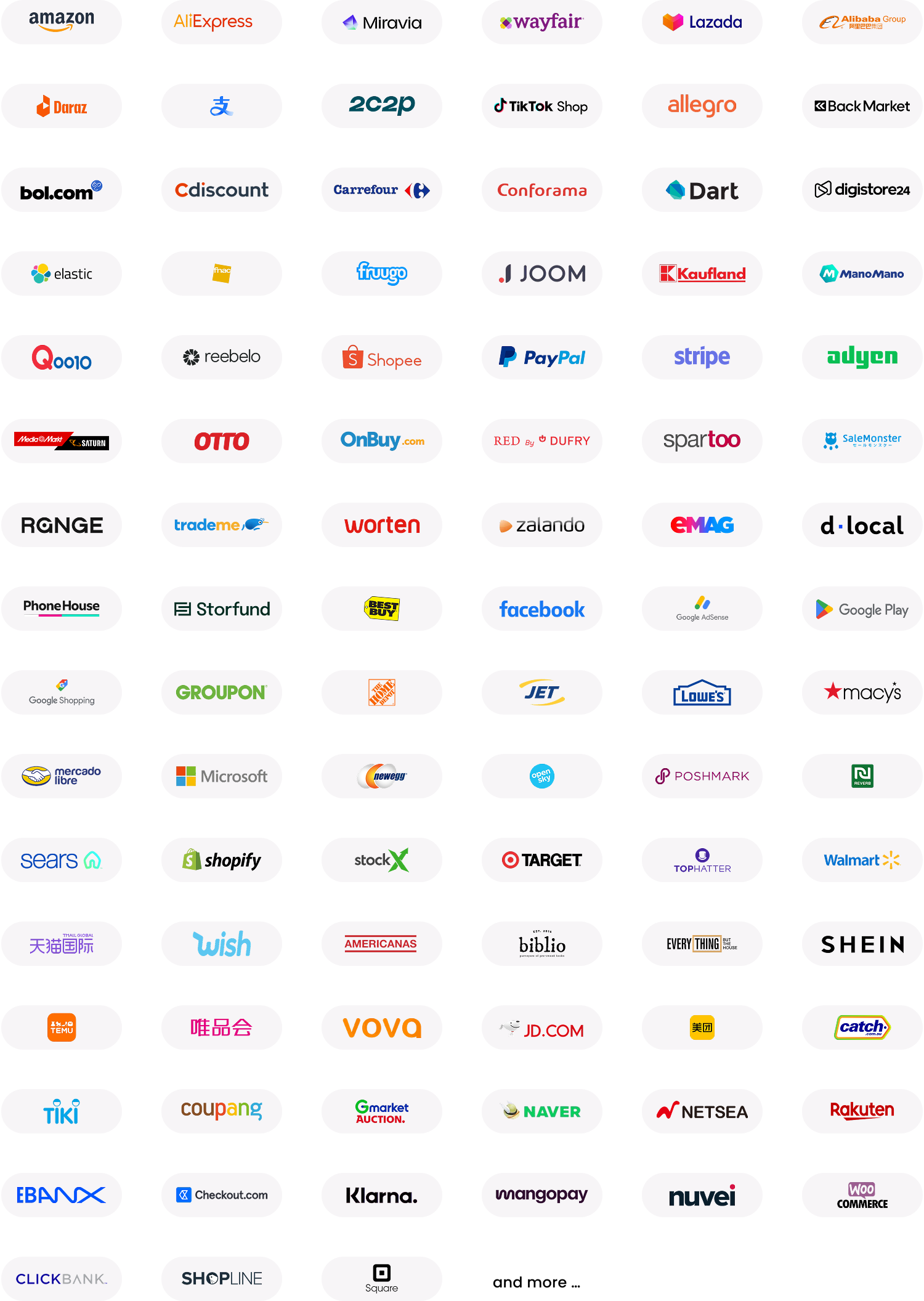

- Collect payments for free from 130+ marketplaces and payment gateways, including Amazon, Etsy, PayPal and Shopify

- Save with competitive exchange rates on currency conversions and transfers

- Lock in exchange rates for up to 24 months for cash flow certainty

Practical tips for the year ahead

Taking steps now to plan and adapt will set you up for the challenges and business development opportunities 2025 might bring. Whether it’s locking in exchange rates, rethinking priorities or exploring new markets, the key is to be proactive and strategic.

Partnering with an expert in cross-border business, like WorldFirst, can make this process simpler. We’ve supported over a million SMEs and enterprises globally to expand their businesses, with tools and expertise to help you manage international payments, reduce currency risks and access opportunities in new markets with confidence.

Get in touch by email or call 020 7801 1065 to see how we can help your business in the new year.

How to sell on Temu: A guide to global success

Discover all you need to know to sell on Temu. We cover creating a profile, selling globally and choosing a multi-currency account that can support you...

Apr / 2025

How to get your Etsy listing on the first page

Learn how to perfect your product listings for Etsy’s search engine and make sure your store isn’t overlooked by customers.

Apr / 2025

How to Set Up Your AliExpress Dropshipping Business

Learn about how dropshipping works, why source goods from AliExpress and how to grow your dropshipping business

Mar / 2025WorldFirst articles cover strategies to mitigate risk, the latest FX insights, steps towards global expansion and key industry trends. Choose a category, product or service below to find out more.

- Almost 1,000,000 businesses have sent USD$300B around the world with WorldFirst and its partner brands since 2004

- Your money is safeguarded with leading financial institutions