Home > blog > Foreign Currency Exchange > Risks of starting a business: 10 common pitfalls + practical fixes

Risks of starting a business: 10 common pitfalls + practical fixes

Last update:

Regardless of the industry, many new businesses face common difficulties. Discover our top 10 and learn what to look out for as you get started.

Launching a business remains one of the most compelling ways to generate value, innovation and independence. But for entrepreneurs, the risks of starting a business are real, multi‑dimensional and often underestimated. Understanding those risks, from financial to strategic, regulatory to technological, can mean the difference between surviving and failing. In this article, we’ve covered the 10 most common:

- Managing cash flow

- Finding your niche and marketing your value

- Ineffective sales funnel

- Competition

- Lack of scalability

- Overcoming red tape

- Operational challenges

- Entrepreneurial burnout

- Opting for quick sales tactics rather than long-term development

- Expansion into a new market

Quick answer:

The risks of starting a business are real – from cash flow gaps and unclear market fit to burnout and limited scalability. But each one can be managed – by forecasting and planning or building a stronger sales funnel and focusing on lifetime value (LTV). That way, you enter new markets with a clear plan.

1. Managing cash flow

Cash flow management is an especially acute risk when starting a new small business. Recent data shows that poor cash flow renders as much as 82% of new small businesses unsustainable within their first five years.

Why does it matter?

Even the best product can fail if the business cannot sustain operations until product‑market fit and scaling.

Two main factors cause failure to manage cash flow properly:

- Failing to raise cash when businesses need it (either from debt/equity financing or improving sales revenues) or

- Failing to cut excess expenditure

Solid cash flow management is critical because small business owners need the flexibility to direct capital at short notice, primarily to meet unexpected investment needs. Without cash to underpin advertising campaigns or inventory turnover, businesses quickly struggle to function.

Signs and data:

- Many small businesses cite “lack of capital or cash flow” as a top challenge.

- A 2025 survey found 36% of US small business owners underestimated costs / mismanaged cash flow in the launch.

Here are some mitigation actions to consider:

- Build conservative financial models (worst‑case, base, best‑case)

- Secure enough runway (12‑18 months minimum in many high‑burn sectors)

- Manage customer acquisition cost (CAC) vs (LTV) for your business

- Monitor burn rate and runway weekly or monthly

- Raise contingency buffer or stagger milestones

Consider whether modern accounting solutions can help illuminate cash flow issues in your business and speak to your accountant about investment strategies.

2. Finding your niche and marketing your value

A second risk of starting a new small business is in meeting the demands of the market, specifically finding its niche and demonstrating its value. Failing to find a successful niche was a common reason for startup failure in a recent analysis by Investopedia.

When conducting market research, there’s often an element of subjectivity over the results. You, as a business, need to pay attention to customers’ genuine needs and wants, positioning yourself to meet these needs and quickly demonstrate the value you offer. Both steps are critical to avoid this particular risk.

Failing to find a niche or market (by ignoring or misunderstanding customers’ feedback) can result in poorly optimised products, while a lack of customer interest can result in low sales revenues and cash flow problems.

Here’s how to fix this:

- Do thorough market research before selling: target customer, pain‑point validation, and willingness‑to‑pay

- Track usage metrics early (activation, churn, retention, sales, etc.)

- Monitor competitor moves and differential advantage

- Be ready to pivot product/market or even business model if early indicators are weak

3. Ineffective sales funnel

Even once you’ve captured your customers’ attention and they’ve understood your value, you need to ensure you’re constantly generating sales. Otherwise, new small businesses risk becoming complacent. If you find that your conversion rate is low, you’re not alone: the average cart abandonment rate according to Statista data is over 70%.

Unfortunately, e-commerce businesses don’t have the benefit of well-trained sales staff that can tailor sales strategies to each new customer. Instead, e-commerce businesses have to rely on content marketing strategies and website design to entice customers into purchasing.

Seemingly small factors like the number of steps in a transaction or the way delivery information is conveyed to customers can drastically increase cart abandonment rates.

Here are some mitigation steps to implement:

- Audit your funnel using analytics: Use Google Analytics, Hotjar, or FullStory to pinpoint high-exit pages, cart drop-off points, and session duration trends

- Simplify checkout steps: Reduce friction by minimising the number of required fields, enabling guest checkout, and clearly showing total cost (with shipping) upfront

- Improve page speed: A delay of even 2–3 seconds can drastically reduce conversions – optimise images, scripts, and use a CDN for faster loading

- Use urgency and trust signals: Add low-stock indicators, countdown timers, and verified customer reviews to prompt faster decisions

- Offer multiple payment options: Integrate digital wallets (Apple Pay, PayPal, Klarna), especially for mobile-first customers

- Set up retargeting: Run dynamic retargeting ads (Facebook/Google) for users who abandon carts or visit product pages but don’t convert

- Optimise product copy: Focus on benefits over features, use SEO-rich language, include high-resolution images and video, and address common objections in FAQs

4. Competition

Another risk to small businesses is fierce competition, especially if your business is up against larger organisations with more resources. The latest ONS figures show that e-commerce is an exceedingly popular industry to enter, coinciding with the recent uptick in online sales.

When finding and demonstrating your business’s niche, it’s not enough to only consider how customers can understand your value. Small businesses also need to convey why they’re more valuable than their competition, too. This nuance should feature in your marketing strategy so customers can better understand their options and identify you as the best.

5. Lack of scalability

E-commerce businesses rely on a high volume of sales to remain viable, so scalability is key. But premature scaling can burn cash and collapse operations. Failing to scale leaves you out‑competed and certain product categories or services have limits. E-commerce businesses with a bespoke or local focus are particularly at risk, as well as software providers with a small user base or ‘freemium’ business model.

If you’re keen to increase your revenue but are finding that your market size is capped, consider where you can diversify products and services and maintain new revenue channels. Diversifying your business can help you avoid over-investing in a single product and maintain your existing customer base while you expand to find new ones.

Here are the mitigation actions to implement:

- Validate product‑market fit before scaling heavily

- Use incremental scaling: test regional expansions, pilot customer segments

- Build scalable infrastructure from day one (website, shopping app, etc.)

6. Regulatory and legal risk

Regulatory issues can impose fines, shut down business lines, or result in reputational damage. Unlike competition from market forces or poor management choices, governments and regulatory bodies place hard requirements on businesses’ profits and policies. Violating regulations (even accidentally) can cause immense trouble for new small businesses. The “Top business risks for 2025” list flags regulatory change as a major risk.

Therefore, new entrepreneurs must familiarise themselves with the legislation that governs their business, including customs processes, tax rates and deadlines, consumer protection legislation, and safety requirements.

Here are some mitigation actions you should implement:

- Begin by speaking with your lawyer and accountant to understand where your business might be vulnerable to legislative requirements and make sure you’re compliant.

- Build compliance into product design (privacy by design, data governance).

- Stay updated on upcoming regulation changes (e.g., EU AI Act).

- Create risk registers for regulatory scenarios and plan for licences, certifications, audits.

- Ensure robust contracts with partners that shift liability appropriately.

7. Operational challenges

Like cash flow management, operational challenges in business are an ongoing issue that small business owners need to contend with. Even a good market fit requires smooth operations – otherwise, customer satisfaction, cost, and timelines suffer.

Operational management concerns how you run your business: whether it’s efficient and whether you’re spending time in your organisation effectively. New small businesses risk being outcompeted by industry peers and losing time to tasks that, nowadays, should be automated.

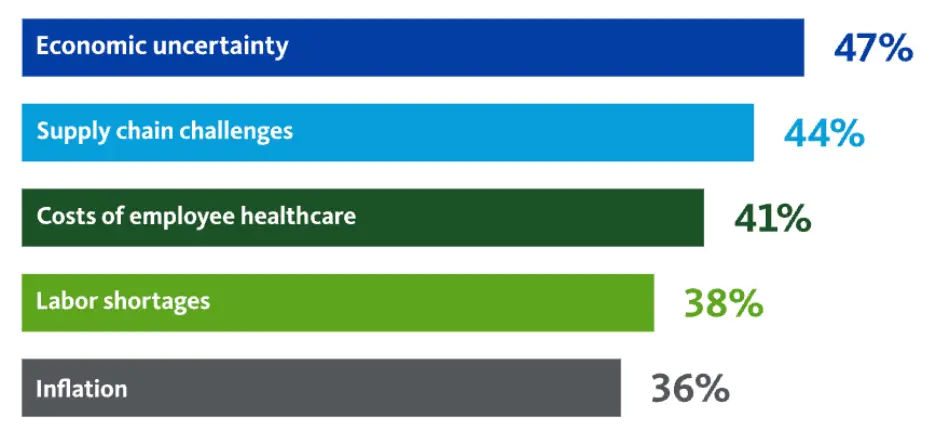

Facing this modernity is concerning for small business owners, and understandably so. The Sentry survey found that 44% of business leaders cited supply-chain/operational challenges as a top risk.

Fortunately, e-commerce businesses have a wide range of options that can increase their efficiency while being cost-effective and easy to implement. These systems include inventory management software that can automate orders and predict optimum stock levels, automated customer emails for abandoned carts and relationships with fulfilment centres to help alleviate logistical pressures.

Here are the mitigation actions to implement:

- Build redundancy in critical systems (technology, vendors)

- Document and standardise processes from Day 1

- Establish SLAs (service‑level agreements) with vendors and have fallback plans

- Hire for quality early: ensure you have experienced operations support, customer success

- Monitor operations KPIs: downtime, customer complaints, churn, performance

8. Entrepreneurial burnout

Starting a business is stressful and draining. That’s why new small business owners need to prioritise the sustainability of their efforts in growing their business or risk entrepreneurial burnout before their new small business becomes established.

Mental health issues resulting from high, sustained stress affect roughly 72% of business leaders (compared to around 48% of the general population). Fortunately, noticing the signs can help you alleviate the pressure.

You can’t run a successful small business without a clear head. If you’re noticing yourself as irritable, tired or forgetful, try to make time for yourself and get disciplined about the amount of rest you need.

9. Opting for quick sales tactics rather than long-term development

Certain tactics within the e-commerce space, like dropshipping, are risky as they prioritise short-term gains rather than long-term sustainability.

New dropshipping businesses lack control over their product’s development and quality and face scarce regional sales exclusivity, leaving them vulnerable to fierce competition. Similarly, the dropshipping business model struggles almost immediately after just a few missed marketing choices.

Despite this adversity, dropshipping is flourishing and can be highly profitable, so if you’ve got a dynamic understanding of evolving consumer tastes, it could prove to be a lucrative endeavour.

10. Expansion into new markets

With global economic forecasts predicting growth for the next five years, small businesses should consider how they can expand into new markets to capitalise.

While there are risks associated with the move for new small businesses, including new cultural customs to learn and legal frameworks to abide by, operational complexities have become more streamlined than ever.

WorldFirst offers small businesses the ability to save time and money when managing their international payments and currency transfers. With over 100+ different currencies to choose from and same-day payment options available, it’s easy to access growing markets and build international supplier relationships.

Make cash flow more predictable from day one. Open a WorldFirst account for free to hold and pay in multiple currencies, send same-day supplier payments, and lock in FX for up to 24 months.

FAQs

What are the biggest risks of starting your own business?

Cash flow gaps, unclear market fit, leaky sales funnels, competition and compliance are the most common early risks.

What is the number one reason small businesses fail?

Cash flow problems – usually a mix of slow collections, poor forecasting and unexpected costs.

How can I reduce the risks of starting a small business?

Start by getting a clear idea of your cash flow – how much is coming in, going out, and when. Make sure there’s a real demand for what you’re selling and build a simple, focused way to attract and convert customers. Understand the rules and regulations that apply to your business. Finally, streamline your operations from day one, so you can automate and scale.

Is expanding to new markets risky for small businesses?

Yes, laws, taxes, logistics, culture, and currency introduce complexity. Use a clear checklist and stage your rollout.

Lawrence Bennett is UK Country Manager at WorldFirst. He brings 15+ years of experience across fintech, ventures and e-commerce.

Lawrence Bennett

Author

Continue reading

Subscribe

The Weekly Dispatch

Get the latest news and event invites. Signup for our weekly update from the worlds of fashion, design, and tech.

You might also like

Choose a product or service to find out more

E-commerce guides

Doing business with China

Exploring new markets

Business Tips

International transactions

E-commerce expansion guides